Exhibition Sector: From Survival to Revival – The Big Screen Comeback Story

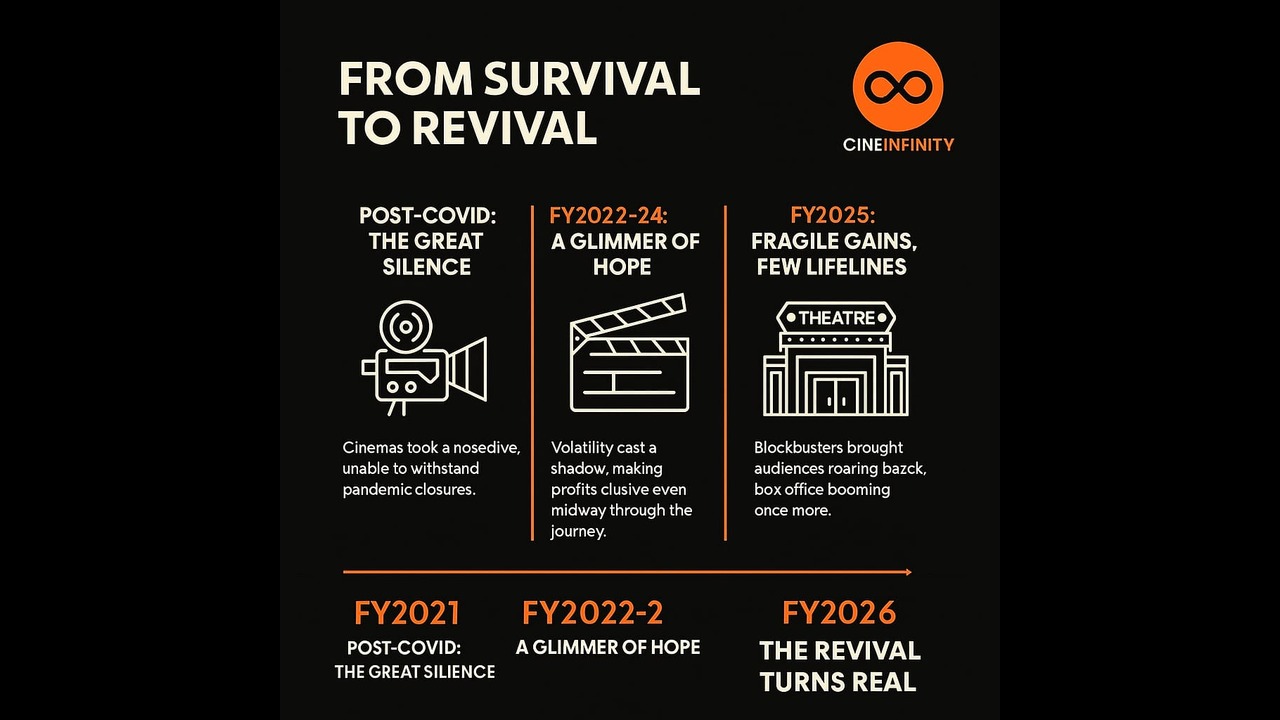

Post-COVID: The Great Silence

When COVID-19 struck, Indian cinemas- multiplexes and single screens alike- went dark overnight. Theatres shut for months, few closes permanently and audiences got used to the convenience of OTT platforms. It wasn’t just a pause, it was a seismic shift.

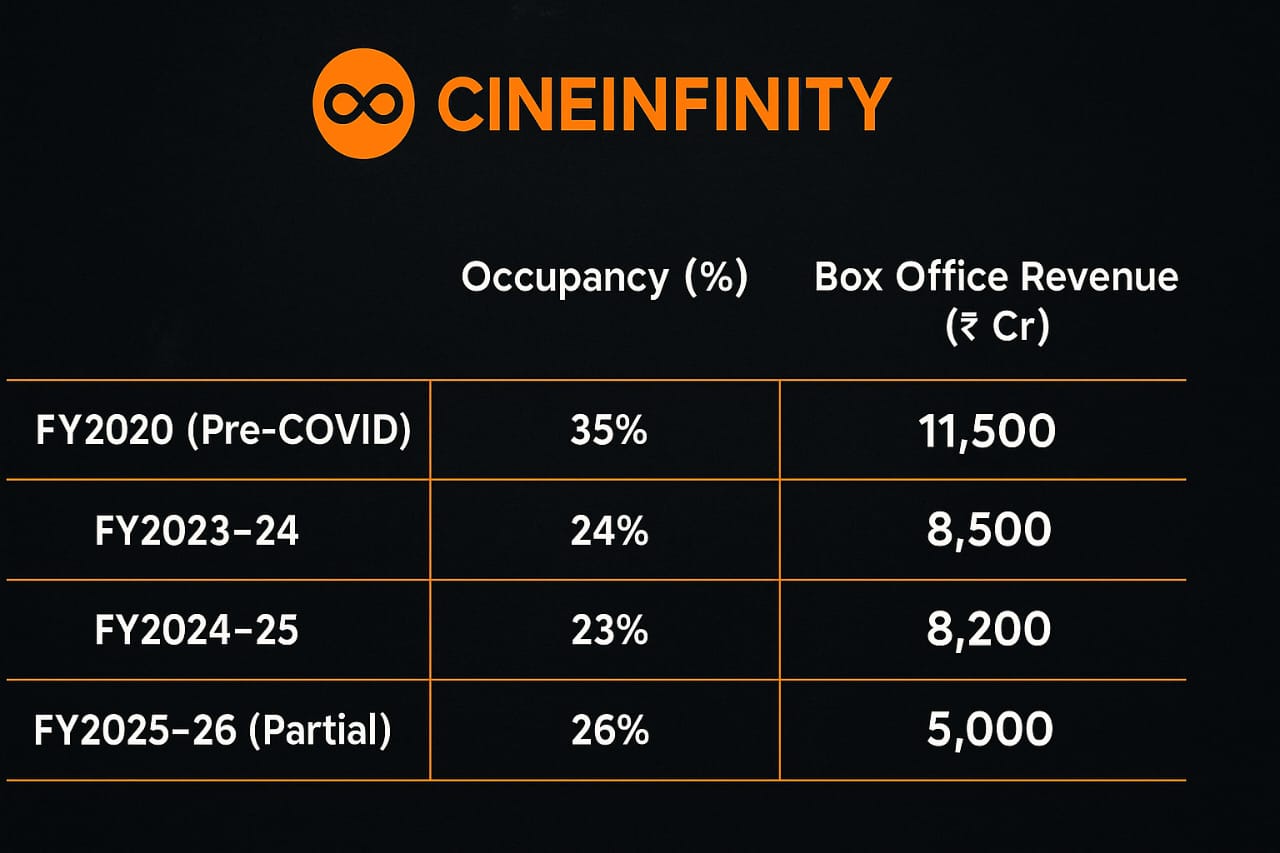

Occupancy rates, which once averaged 34.9% in the pre-pandemic era (FY2020), plummeted to the low 20s in the years after reopening. Rising operational costs, stagnant ticket pricing in some markets, and the pull of streaming meant profitability was nowhere in sight.

2023–24: A Glimmer of Hope

The tide began to shift in FY2023–24. Big-budget spectacles like Pathaan, Jawan, Gadar 2, Jailer, and Animal brought audiences back in droves, if only temporarily.

Multiplex chains like PVR-INOX posted annual occupancies in the 22–25% range, still far from pre-COVID benchmarks but an improvement over the barren pandemic years.

However, the recovery was fragile. The hits were huge but the misses were costly. Without consistent content, exhibitors still couldn’t find stable ground.

2024–25: Fragile Gains, Few Lifelines but Not at all Good Year.

The year started on a worrying note. Content volatility and a soft slate meant Q4 FY2025 saw occupancy dip to 20.5%, admissions fall 6.3%. Losses widened to 1.06 billion for PVR-INOX in that quarter alone.

Yet, a few titles prevented the year from being a complete washout. Pushpa 2 and Stree 2 delivered “Blockbuster” numbers, ensuring cinemas stayed relevant.

2025–26: The Revival Turns Real

Then came the spark the industry was waiting for.

Q1 FY2026 (Apr–Jun 2025) marked a genuine turnaround:

Footfalls grew 12% YoY

Ticket prices rose 8%.

Net losses halved to 540 million from 1.79 billion the year before

This wasn’t just luck- it was the result of content consistency across languages and genres.

Blockbusters Powering the Bounce

Saiyaara – YRF breakout hit: 83 crore opening weekend, holding steady for weeks, eyeing 350 crore lifetime.

Mahavatar Narsimha – The highest-grossing Indian animated film ever at 150 crore only in hindi.

Chhaava, Sitaare Zameen Par, Raid 2- Mid-year successes that kept multiplexes buzzing.

By June 2025, India’s box office had already crossed 5,000 crore for the year- A 27% jump YoY and the strongest first half in over half a decade.

Q2 2025–26: From Dull to Dominant

Mid-year industry mood was cautiously optimistic. Q2 was expected to slow down… until the release lineup flipped the script:

August: War 2, Coolie, Param Sundari

September: Baaghi, Jolly LLB 3

Suddenly, August and September looked like back-to-back goldmines. If trends hold, FY2025–26 could surpass the combined box office of the last five years—a milestone no one imagined possible during the dark COVID months.

Beyond the Big Cities

One key change in the recovery playbook:

Multiplexes are expanding aggressively into Tier II & Tier III cities, which now account for about 22% of PVR-INOX’s screens. Lower real estate costs, less OTT penetration, and community-driven entertainment habits make smaller towns an untapped goldmine.

Screen Count: India vs. Global Peers

India’s screen infrastructure lags globally:

India: 9,000–10,000 screens in total (5,500 single-screen + 4,000 multiplex screens)

USA: 40,000 screens

China: 86,000+ screens

On a screens-per-million metric:

India: 7–8 screens per million

China: 30 screens per million

USA: 125 screens per million

The Road Ahead

The Indian exhibition sector still faces headwinds OTT competition, high operational costs and the unpredictability of content performance. But for the first time in years, momentum is on its side.

With a strong Q2 slate, a festive season packed with potential blockbusters and a newfound audience appetite for the theatrical experience, FY2025–26 could mark the industry’s most profitable year since pre-pandemic highs.

If the last few years were about survival, the next few could be about dominance. The big screen isn’t just back- it’s ready for its biggest close-up yet.

If the last few years were about survival, the next few could be about dominance.

The big screen isn’t just back — it’s ready for its biggest close-up yet. Because the magic of the Big Screen, the grandeur of 70MM is timeless and the industry’s next act promises to be bigger, brighter and bolder than ever.